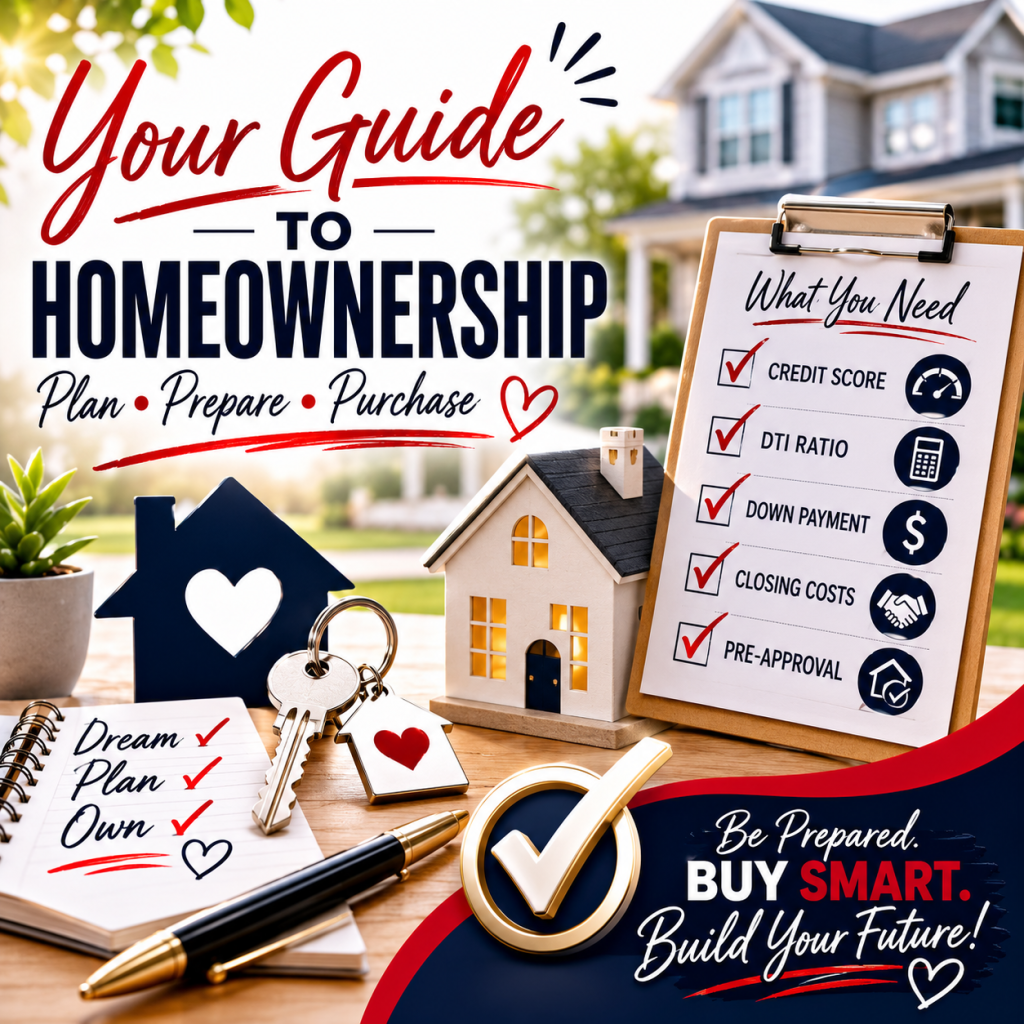

Buying a home is one of the biggest financial decisions you’ll ever make. Whether you’re a first-time buyer or returning to the market, understanding the mortgage process can help you avoid surprises and position yourself for success.

This guide will walk you through the key factors lenders consider when determining whether you qualify for a home loan.

Step 1: Understand Your Credit Score

Your credit score is one of the most important factors lenders review.

General Credit Score Guidelines

| Loan Type | Typical Minimum Score |

|---|---|

| FHA Loan | 580+ |

| Conventional Loan | 620+ |

| VA Loan | Varies by lender (typically 580-620+) |

| USDA Loan | Usually 640+ |

A higher credit score can help you:

- Qualify for better interest rates

- Lower your monthly payment

- Reduce mortgage insurance costs

- Increase your purchasing power

Before Applying

Avoid:

- Opening new credit cards

- Financing furniture or vehicles

- Missing payments

- Closing old credit accounts

Do:

- Pay all bills on time

- Keep credit card balances low

- Review your credit report for errors

Step 2: Know Your Debt-to-Income Ratio (DTI)

One of the most misunderstood parts of the mortgage process is DTI.

DTI stands for Debt-to-Income Ratio.

This number compares your monthly debt payments to your gross monthly income.

Example

Monthly Income:

$5,000

Monthly Debts:

- Car Payment: $400

- Student Loans: $200

- Credit Cards: $100

Total Monthly Debt:

$700

DTI Calculation:

$700 ÷ $5,000 = 14%

DTI = 14%

Why DTI Matters

Lenders want to make sure you can comfortably afford a mortgage payment.

Generally:

- Under 36% = Excellent

- 37%-43% = Good

- 44%-50% = May still qualify depending on the loan

- Above 50% = Often difficult to qualify

Step 3: Save for Upfront Costs

Many buyers focus only on the down payment, but there are other expenses involved.

Down Payment

Down payment requirements vary.

FHA Loan

Typically 3.5%

Conventional Loan

As little as 3% for qualified buyers

VA Loan

Often 0% down for eligible veterans

USDA Loan

Often 0% down in eligible areas

Step 4: Understand Closing Costs

Closing costs are separate from your down payment.

They typically range from 2% to 5% of the purchase price.

Closing Costs May Include:

- Loan origination fees

- Appraisal

- Home inspection

- Attorney fees

- Title fees

- Recording fees

- Property taxes

- Homeowners insurance

Example:

$300,000 Home

Closing Costs:

Approximately $6,000-$15,000

Many buyers are surprised by this expense.

The good news is that some sellers and builders offer closing cost assistance.

Step 5: Build Your Savings

Even if you qualify for a mortgage, lenders like to see financial stability.

Try to maintain:

- Emergency savings

- Consistent income

- Stable employment history

- Money remaining after closing

Homeownership comes with unexpected expenses.

A healthy savings account can help you handle:

- Repairs

- Maintenance

- Appliance replacement

- Deductibles

Step 6: Employment Matters

Most lenders prefer:

- Two years of employment history

- Stable income

- Consistent earnings

This doesn’t mean you cannot change jobs. However, major career changes should be discussed with your lender before applying.

Step 7: Avoid Major Purchases Before Closing

Once you’re pre-approved, do not:

❌ Buy a car

❌ Finance furniture

❌ Open new credit cards

❌ Co-sign for someone else

❌ Make large unexplained deposits

Any of these actions could impact your loan approval.

Step 8: Get Pre-Approved First

Before shopping for homes, obtain a mortgage pre-approval.

A pre-approval helps you:

- Understand your budget

- Strengthen your offer

- Identify potential issues early

- Shop with confidence

Most sellers prefer offers from pre-approved buyers.

Common Homebuyer Myths

Myth #1:

“I need 20% down.”

Truth:

Many buyers purchase homes with much less.

Myth #2:

“My credit must be perfect.”

Truth:

Many loan programs allow less-than-perfect credit.

Myth #3:

“I should wait until rates drop.”

Truth:

The right time to buy depends on your financial readiness, not just interest rates.

Myth #4:

“Renting is always cheaper.”

Truth:

Rent payments build your landlord’s wealth. Mortgage payments build equity for you.

Ready to Become a Homeowner?

The path to homeownership starts with preparation. Understanding your credit, managing your debt, saving for upfront costs, and working with experienced professionals can make the process much smoother.

If you’re thinking about buying a home in Georgia or Alabama, I can help connect you with trusted lenders, explain your options, and guide you through every step of the homebuying journey.

Contact LaKeisa Rucker

Real Estate & Styles

Serving Georgia Homebuyers

Leave a comment